Nearly half of the estimated online gaming revenue generated from Philippine players in the first quarter flowed through offshore operators that by definition are not subject to local licensing. That is according to artificial-intelligence (AI) -powered insights from Blask, an analysis platform covering the gaming sector.

Projected revenue, measured via what Blask calls the competitive earning baseline (CEB), reached US$1.17 billion at midpoint, across what it said were “257 active operators”. That was up 32 percent versus first-quarter 2025.

Blask describes CEB as an AI-driven projection of the realistic gross gaming revenue (GGR) a brand should capture in a specific market, rather than a standard internal profit-and-loss metric.

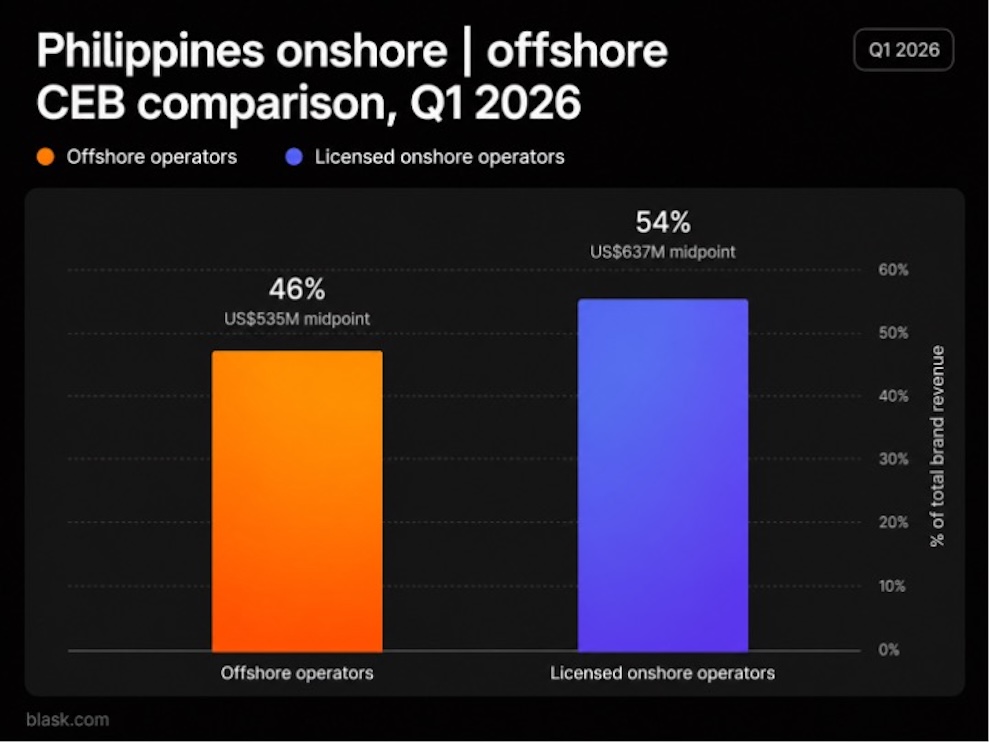

It stated that for the three months to March 31, offshore operators addressing the Philippine market “accounted for an estimated 46 percent of projected brand revenue… equivalent to approximately US$535 million at the midpoint.”

Blask added, referring to online operators approved by the Philippine Amusement and Gaming Corp (Pagcor): “Licensed onshore operators contributed the remaining 54 percent, or roughly US$637 million.”

Blask noted in an analysis briefing shared with GGRAsia, that the revenue-split between offshore and onshore operators had shown “narrowing” over the quarter.

It stated: “In January, onshore and offshore revenue stood close to parity (51 percent/49 percent). By March the gap had widened to 58 percent/42 percent in favour of licensed operators.”

The analytics brand said some divergence in Pagcor data on online gaming demand and the figures observed by Blask, could to some extent be assigned to differences in reporting scope.

Blask said that while from its analysis, first-quarter consumer demand for online gambling brands in the Philippines “rose sharply” over the same period, Pagcor reported a 15.9 percent year-on-year decline in aggregate GGR, to PHP87.60 billion (US$1.42 billion).

The decline was driven by Pagcor’s defined electronic gaming segment – “e-bingo, e-games, and bingo grantees” – which fell 22.4 percent year-on-year to PHP39.90 billion.

Blask said the divergence reflects a difference in scope in reporting methods.

“Pagcor’s figures capture its licensed operator framework and land-based venues, while Blask tracks consumer-facing digital demand – including offshore brands that fall outside Pagcor’s reporting perimeter,” it explained.

Blask Index – the platform’s measure of brand demand – nearly tripled year-on-year for the Philippine market in the three months to March 31.

The analytics firm also said that what it describes as top 10 brands by Brand’s Accumulated Power (BAP) “show a clear pattern”. BAP is defined as a brand’s share of total market demand in a given country and period.

According to Blask’s data, “seven of the top eight operators posted year-on-year Blask Index growth above 400 percent, with three exceeding +3,000 percent”.

“All eight top-ranked brands operate under a Pagcor licence, while the remaining two… are offshore and both declined year-on-year,” the firm noted.

“This points to competitive redistribution within the licensed segment rather than uniform market expansion,” it added.